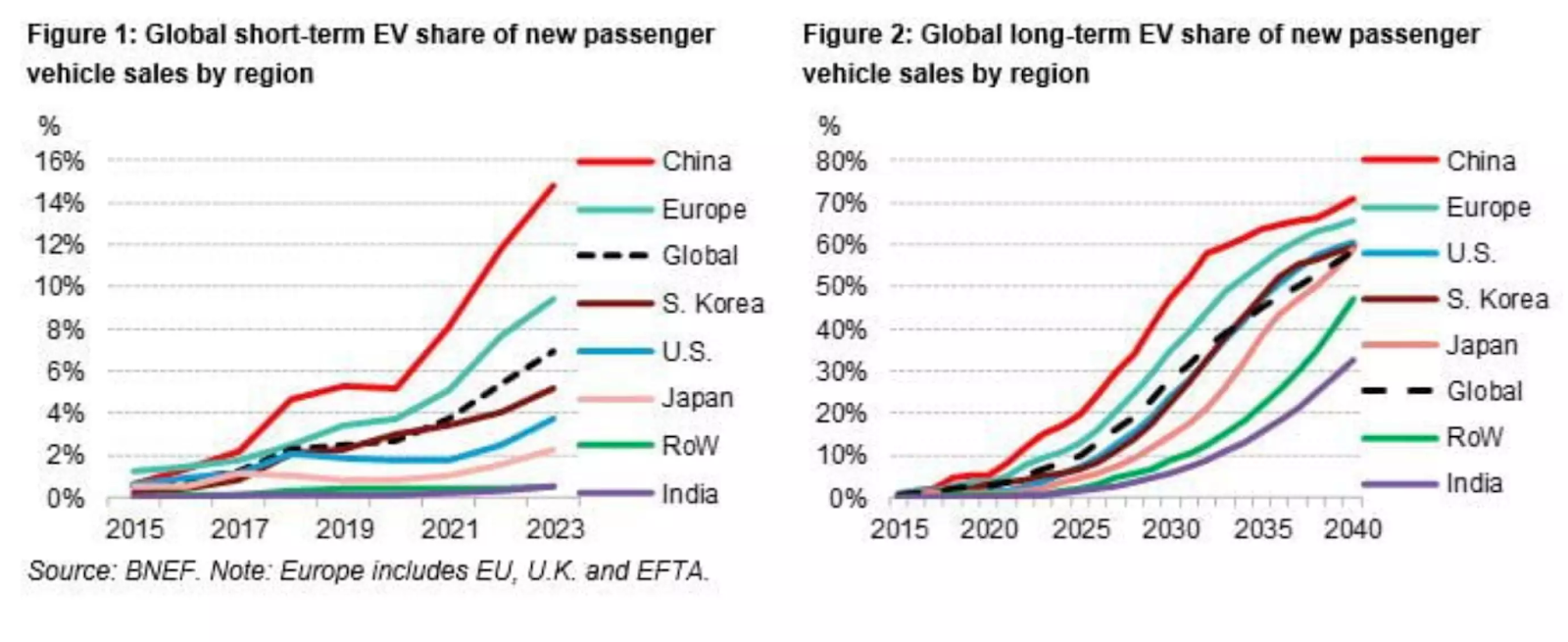

The Automotive Industry stands at a huge Turning Point. Fuel prices are at an all time high and urban air quality at an undeniable low. The only way forward is to convert all our energy production to zero emission renewable sources and our Internal Combustion Engine (ICE) vehicles to Electric Vehicles (EVs). EVs use electricity obtained from the grid to charge batteries that then supply power to the wheels via a motor. Tesla popularized the EV in the USA over a decade ago and since multiple companies across the world have created different solutions. The process of adoption of EVs across the world is rapidly growing with China (13%) and Europe (16%) taking the lead.

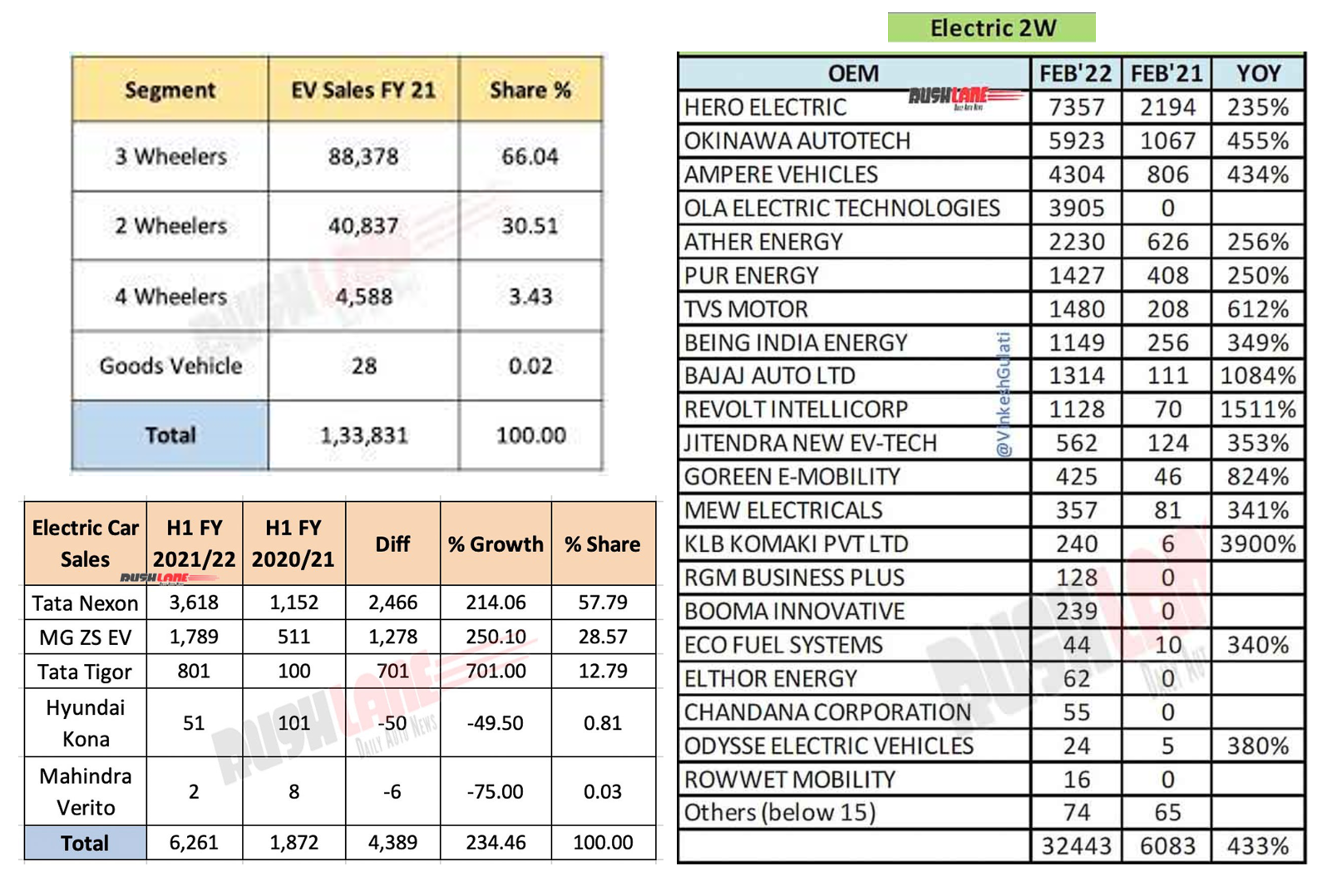

India today has a 1% EV Market share but is seeing a massive increase in the interest and demand for EVs. Over 3 Lakh vehicles were sold in 2021-22, a growth of 160% over 2020-21. India's EV market size is expected to reach USD 152.21 billion by 2030, expanding at a CAGR of 94.4% from 2021 to 2030. A majority of these Vehicles will use Lithium Ion (Li) Batteries and will require a personal or public charger station to refuel their batteries.

Market Trend

By 2025, India is expected to have over 5 million EVs. The increasing demand is mainly a result of government subsidies, rising gas prices and an overall acceptance of EVs as being an effective solution for daily use.

Fig. 2: Sales in India of 2, 3 and 4 Wheelers in FY 20, 21, 22 (Credit: Rushlane)

Based on demand and projections, the EV sector in India is going to potentially see more than 10% market share for the following product segments:

- Two Wheelers for Urban Commute and Delivery (Rs. 50,000 - 1 Lac)

- Two Wheelers for Personal Commute & Riding Leisure (Rs. 1.2-2 Lacs)

- Three and Four Wheelers for Intra City Commercial Movement (Rs. 3 - 6 Lacs)

- Four Wheeler Sedans for Ride Hailing & SUVs for Personal Use (Rs. 9 - 15 Lacs)

- Intra-CIty Buses for Passenger Commute (Rs. 2 - 2.5 cr.)

Two Wheelers (2Ws)

- 2Ws for Urban Commute will primarily drive the adoption of EVs in India. Ampere, Ather, Hero Electric, Okinawa and Ola Electric have dominated sales and have combined sold over 300,000 scooters in the Low and High Speed Category.

Mass Market Scooters Premium Scooters

Pure, Hero, Okinawa, Ampere Ola Ather

SInce 2021, The Govt. Fame 2 subsidy of Rs. 15,000/kWh is applicable for all 2Ws sold under Rs. 1.5 Lacs. The Low Speed Mass Market category will contribute > 90% of sales and will rely on Sale of 2Ws directly to consumers and fleet operators. From a technology perspective, > 80% of all 2Ws in the Market today are carryovers or re-engineered Chinese systems implemented without any extensive development or validation. To truly earn consumer interest and trust, the Core technology and Software Stack will have to be engineered for Indian road and weather conditions to enable Safe, Reliable operation. The differentiators in the future will be based around Scalability and Performance and companies who develop Affordable, Safe & Reliable systems will stand out.

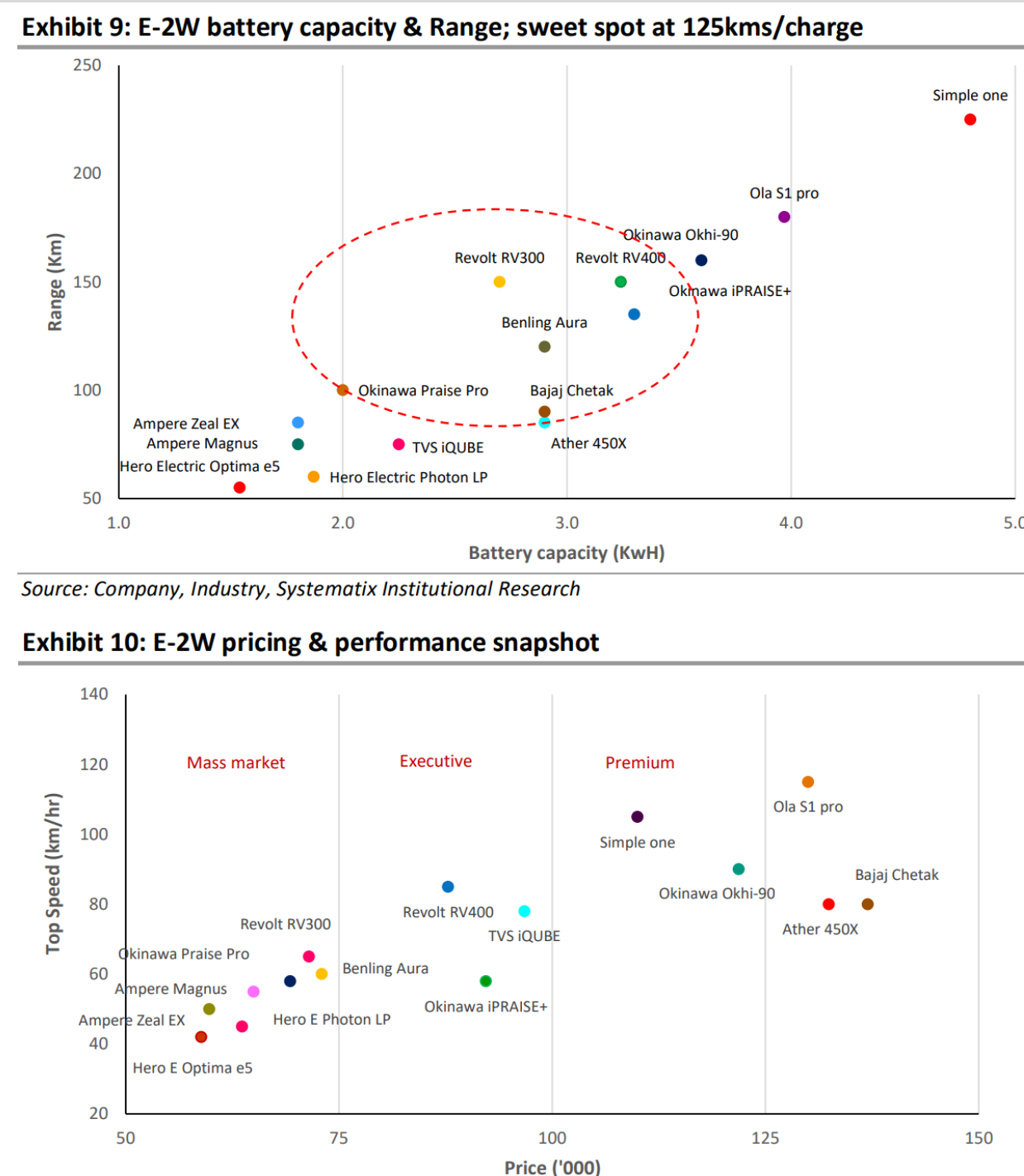

Fig. 4: Price v/s Speed of Two Wheelers sold in India

Few strategies to allow mass scale adoption in the 2 and 3 wheeler sector will be:

- Setting up Interoperable Battery Swap Systems that allow standardized batteries to be used across different vehicles and OEM platforms. These batteries can be removed from the vehicle and swapped with similar batteries within 2 minutes.

- Enabling < 1 hour Charge using standard 15 A Wall Sockets by developing <3 kWh Safe, Fast charge capable Batteries. For users with access to a dedicated 15 A plug point, Portable 1-3 kW chargers will be used in Residential and Commercial areas across cities to charge as per convenience.

- Building High Quality & Robust batteries engineered for Indian conditions. Extreme temperature variations, abusive driving patterns and higher utilization will mean that engineering an indigenous Battery solution will be key. India will primarily rely only on China for Cells for the next 5 years which makes engineering the rest of the battery very crucial, so as to avoid Fire Incidents, Low Life & Poor Charge Speeds.

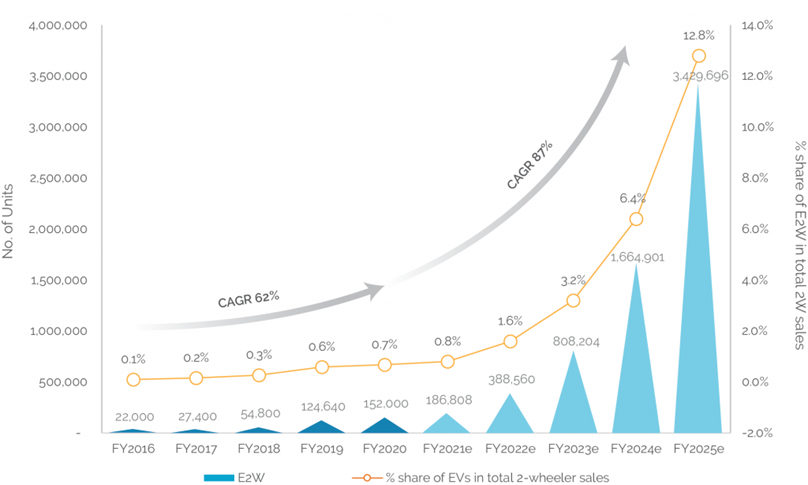

Fig. 5: Growth in Two Wheeler Segment

- Electric Motorcycles built for Highway Riding, Off road Applications & Military Operations will need at least 2 years to perform on par with ICE Vehicles such as the Royal Enfield Classic, KTM Duke or Bajaj Pulsar in terms of Cost, Range, Life and Speed. Today, EV Batteries & Powertrains are at least 30% more expensive when compared to ICE systems and account for > 60% of the price of an EV. Moreover, no subsidy by the Indian Govt. for products priced above Rs. 1.5 Lakhs also means that Companies will have to innovate with their Business Model to have a similar cost price as ICE Vehicles.

There is a growing section of the population who values Sustainability, Performance and Experience. This section is fascinated by Aspirational EVs such as RIvian and Tesla but ride a 2W for Commute and Occasional Leisure. They would pay the Premium if the product and experience lived up to the expectation. Few Companies around the world are attempting to create a Product for this demographic and sell sub $4,000 Motorcycles (Sondors, Ultraviolette, Koltter) but none have been able to achieve production scale or prominence similar to 4 Wheeler counterparts such as Tesla. This therefore allows a $3 Billion opportunity in India and $7 Billion Worldwide by 2026. Factors that will be responsible for the success of EVs in this sector will be:

- Modularity: Enabling multiple product styles (Sports, Retro, Street) on a standard EV platform with minimal parts will be the key to allowing Low Costs & High Margins. Having a lightweight, efficient and modular EV platform will allow scaling across different product and user segments with minimal assembly investments and marginal difference in cost price.

- Battery, Charging Technology: For continuous Highway riding, the Vehicle has to be capable of doing a minimum of 200 kms at highway speeds (70 kph) and >300 kms in the city. This translates to a battery that is a min. 30 kgs in weight thus making it impractical to swap. 3 kW Charging using a standard wall socket will not be enough as it would take over 2 hours to charge 200 kms. Fast charging to enable 300 kms range within 30 minutes using a standard DC01 or CCS2 Charger Network will be key. The Innovations required to achieve the same are not in production yet.

- Positioning: The Design & Brand language has to be extremely definitive as the Future of Riding is going to be very different from what it is today. Gen Z yearns for a stronger personal integration of their aesthetic, attitude and values with the brands they associate themselves with. They are also going to be more drawn to Experiences that merge Sustainability, Community & Virtual Reality. The product also has to offer high performance and safety while being priced between $3,000 - $5,000 (Rs. 2-4 Lacs).

Fig. 6: EV Motorcycles available between $5,000 - $10,000

Production release date and Origin Country mentioned

Light Commercial Vehicles (LCVs)

Low Speed Three Wheelers were the first EV sector to attain mass adoption in India. Almost 500,000 Lead Acid & Li-ion 3Ws are being used for Passenger Transport for the last 5 years but the supply and manufacturing of these has been fractured by quality and reliability issues. Mahindra Treo and Piaggio Ape are some of the major Conventional OEM solutions selling products with most others releasing by 2023. There is also a huge demand from Delivery and Logistics companies to switch to EV fleets to reduce operating cost and carbon footprint. This coupled with the 20% increase in deliveries post COVID make LCV’s a $5 Billion opportunity in India by 2025. The LCV sector will rely on few key enablers for mass adoption:

- Cost: Price will be the biggest factor. Today, the lowest priced 600 kg Load Carrying EV is priced at Rs. 3.5 Lakhs. This, though similar in price to a Tata Ace, has 3 wheels, 15 kph lower top speed and ~150 kgs lower loading capacity.

- Product Efficiency: Range, Life and full load performance will be key parameters. EVs that are able to deliver ~150 kms range at full load capacity while maintaining the lowest possible operating cost and battery size will have an advantage.

- Charging Options: Allowing multi modal charging systems (Swap, Fast Charge and Larger Batteries) will be key as there will be no swap standardization amongst this sector. Based on the use case, users can decide the option for charge accordingly.

There are currently no major technological barriers for adoption and the systems required to enable a Product similar to the TATA ICE ACE within a 15% increment in cost exist today. Multiple products such as the Euler Hiload, Rage OSM and Tata Ace EV (2023) can meet user requirements while allowing lower cost over life. Most companies in this sector will import parts and systems from China for the next few years till supply is set up indigenously. Success in this sector will depend on who can scale manufacturing and distribution quickly and affordably while offering strong after-sales service.

Euler Hiload, Altigreen Neev, Tata Ace EV, OSM Rage

Four Wheelers (4Ws)

Cars and Larger passenger vehicles will require ~3 years to meet cost targets to really enable > 7% Market share. Nexon EV and Tigor EV comprised 96 percent of all sales and have sold a total of 20,000 units since inception in 2020. Tata Motors has ambitious plans to introduce as many as eight new EVs in India by 2025, while Mahindra, Ola and MG have announced plans for multiple new EVs for India starting 2023. Maruti’s first EV for India, to be developed along with Toyota, will potentially start selling in 2025. Other major players such as Hyundai, Kia, Skoda and VW will import parts, assemble in India and sell EVs at a price over Rs. 20 lakhs for the next couple of years. A lot of the EV technology will be based on Joint Ventures and Supplier Collaborations with multiple companies from China, Germany and USA. Multiple companies will be involved in facets such as Charging Setup, Vehicle Management Systems and Connected Car Solutions.

MG ZS, Tata Nexon EV, Hyundai Kona, Tata Tigor EV

Intra-City Buses

India relies heavily on public transportation and going Electric allows one of the largest consumers of Oil to drastically lower operating costs. But the upfront cost being 30% higher has been a huge deterrent. FAME II, with an outlay of INR 10,000 crores, is aimed at providing incentives of up to INR 50 lakhs each for 7,090 e-buses. Bids to procure 5,580 e-buses have recently been sought by CESL and the lowest price discovered for a 12-meter bus is ?43.49 per km, and a 9-m bus is ?39.21 per km. This includes the cost of electricity for charging the buses and works out cheaper than ICE Buses. This itself will enable over $6 billion in sales by 2026. The higher financial entry barrier means that only large firms such as TATA Motors and BYD - Olectra will have the upper hand in the market for the next few years. Dependency on imports, actual vehicle life and lack of charging infrastructure will be the key problems to solve. A considerable amount of work will go into setting up the grid infrastructure required to enable >100 kW Charging levels. There will also be some work across the country to understand the implementation and possibilities of using Hydrogen fueled buses in parallel. The actual long term possibility of using Hydrogen or alternate Fuel Cells for Buses is yet to be seen.

TATA, Olectra, Ashok Leyland and JBM are leading players